8 / 67

8 / 67

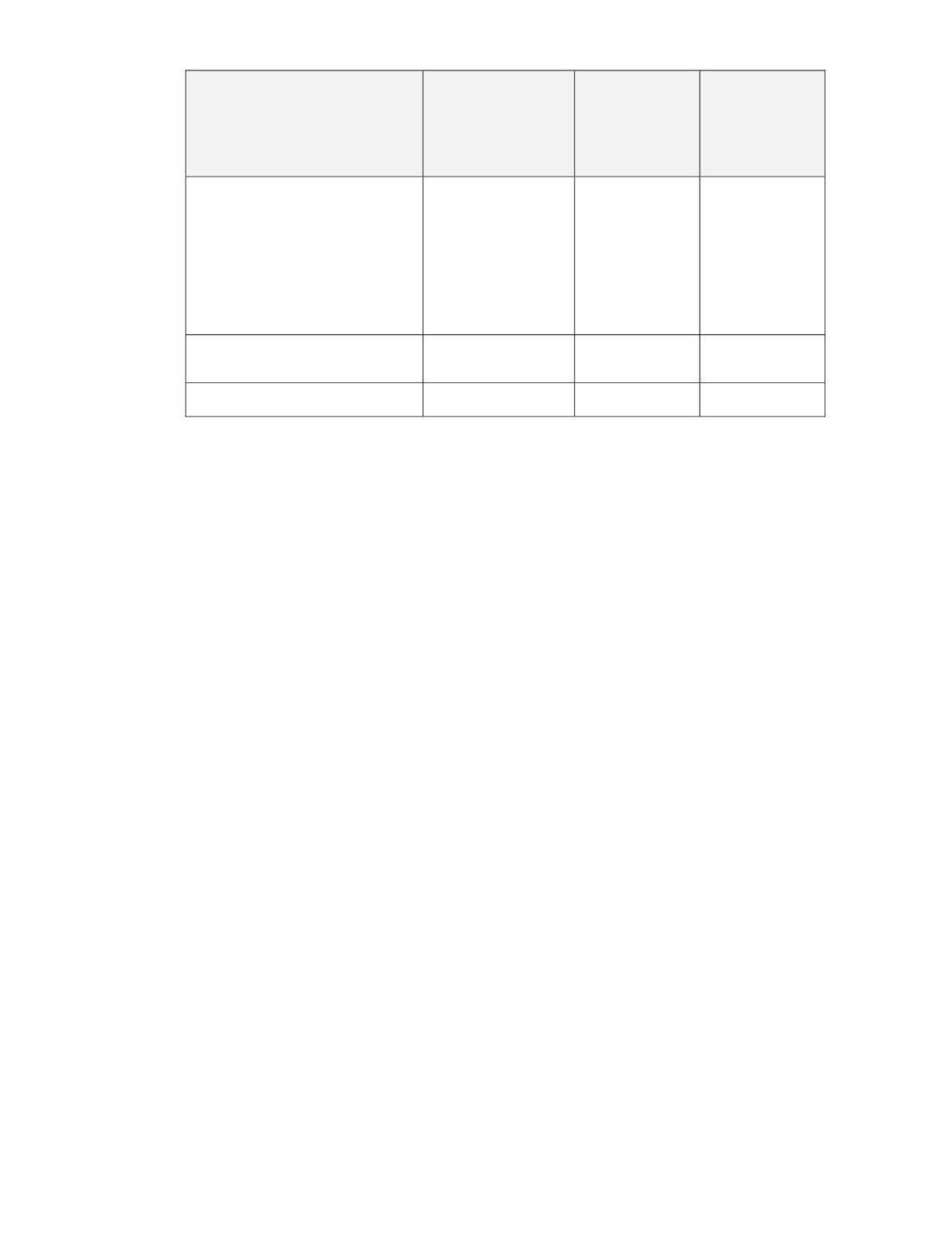

4

Nature of Transactions with the

HEINEKEN Group

Estimated aggregate

value as disclosed in

the Circular to

Shareholders dated

22 March 2017

(RM’000)

Actual value

transacted since

13 April 2017 till

22 March 2018

(RM’000)

Estimated

aggregate value

from 54

th

AGM

to the next AGM

(RM’000)

4.

Fees received / receivable from

the HEINEKEN Group for

professional services which

include market research and

analysis, trade and marketing

advisory, innovation

development and other

support services

31,200

13,950

15,000

5.

Sale of beverage products to the

HEINEKEN Group

20,000

6,417

10,000

Total

139,400

84,205

112,700

None of the actual value of other recurrent related party transactions as disclosed above

has exceeded the estimated value by 10% or more.

All estimated values of the respective Recurrent Related Party Transactions from the date

of the 54

th

AGM to the next AGM are estimated based on the past transactions entered

into by the Group and the Related Parties as well as estimates made based on

management’s projected sales / businesses, orders and agreements. The actual value of

these transactions may vary from the estimated value disclosed below.

As of the financial year ended 31 December 2017, there was no amount due and owing

to the Group by its related parties arising from the Recurrent Related Party Transactions

that exceeded the credit term.

2.4 Guidelines and Review Procedures for Recurrent Related Party Transactions

To ensure that such Recurrent Related Party Transactions are conducted at arm’s length

and on normal commercial terms consistent with the Group’s usual business practices

and policies and will not be prejudicial to the Company’s shareholders, the following

principles will apply:

i)

transactions with the Related Parties will only be entered into after taking into

account the pricing, level of service, quality of product, market forces and other

related factors on terms not more favourable to the Related Parties than those

generally available to the public and not detrimental to the minority shareholders of

the Company;

ii)

transactions with Related Parties will only be entered into under similar commercial

terms for transactions with unrelated third parties, which depend on the demand

and supply of the products and subject to the availability of the products in the

domestic market;

iii)

should a cost plus basis of pricing be used, the appropriate mark-up to cost shall

be determined on an arm’s length price based on a percentage earned by the

Company on unrelated party transactions which are the same or very similar to the

related party transactions;